GUDIES AND EXPLAINERS

With interest rates rising, many borrowers are taking the time to review their home loan arrangements. A review of your loan structure may assist in managing repayments, subject to your individual circumstances.

Retirement often conjures up images of afternoons on a golf course or adventures in a motorhome, of growing your own vegetables or spending quality time with the grandkids.

Negative gearing is a popular investment strategy in Australia, but it’s also a term that often comes up in the media, particularly when there’s an election looming, like right now. Let’s take a look at what it means, what capital gains tax (CGT) is and why you need to know about these terms if you plan to invest in property.

It’s Federal Budget time, so let’s cut to the chase. What’s in it for aspiring homeowners looking to purchase a property in 2025? Here are some of the key takeaways that could affect you.

So, you’ve decided to buy a property. How exciting! Understanding the world of home loans may be confusing like what the difference is between a fixed and variable interest rate home loan. Both home loans setups offer unique advantages and what is better will depend on your situation + objectives. Here are some of the key factors to consider when working out which type of home loan is right for you.

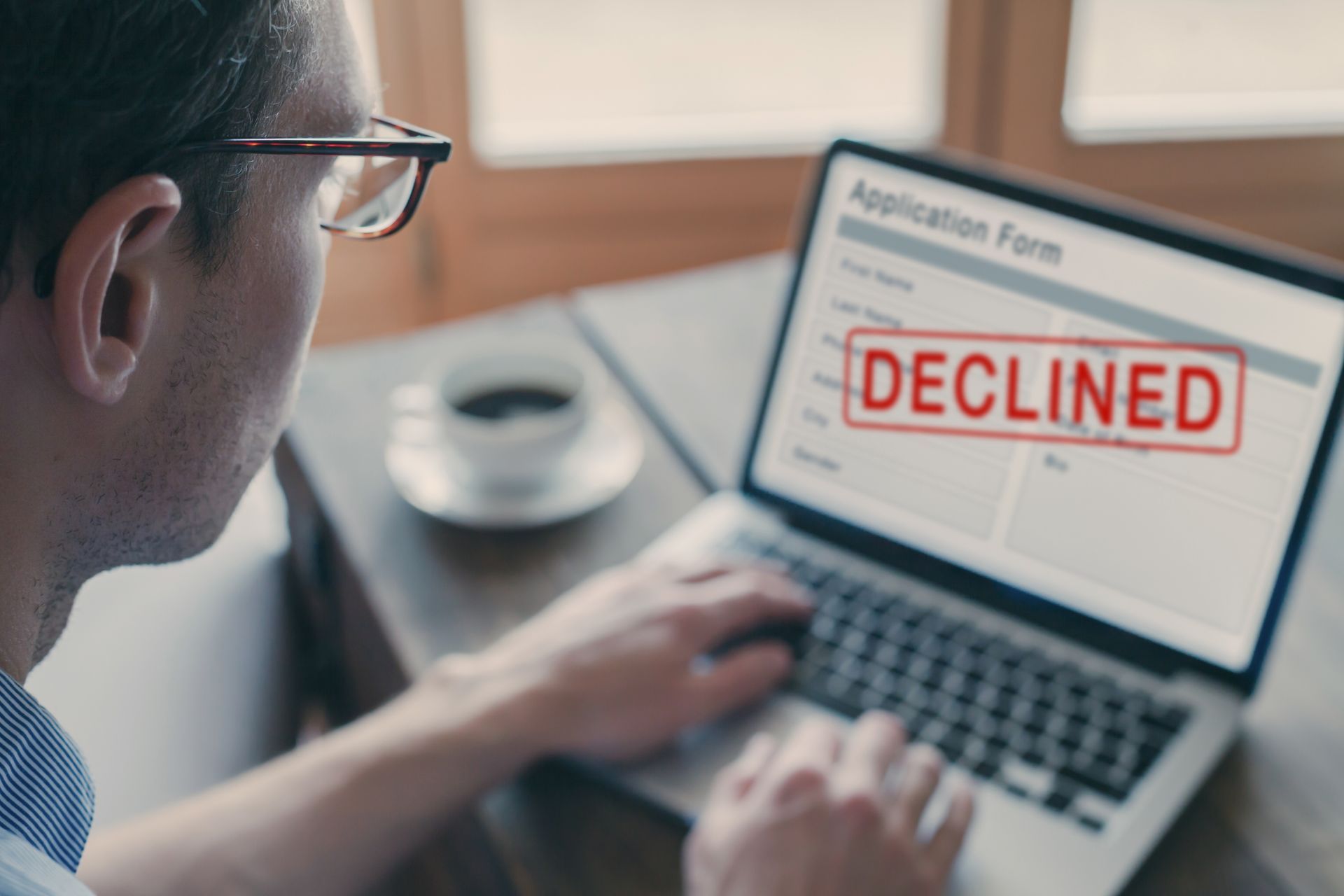

Applying for a home loan is both exciting and stressful. When you are successful, there’s nothing like receiving that green light from a lender to say you’re on the home run to securing your dream home. But it’s important to be aware that even if you do have pre-approval, you can be knocked back for a home loan. Pre-approval is an indication from a lender that they’re likely to approve you for a specific loan, but you still have to meet certain lending conditions. Here are some of the common reasons why a mortgage application may be denied after you’ve been pre-approved, and what to do if you are rejected. Your financial situation has changed A change to your financial situation could impact your home loan application. Maybe you’ve lost your job or are working less since you were pre-approved. Lenders will look at your ability to comfortably repay a home loan, and if your income has taken a hit of late, then you may be rejected. Likewise, if you’ve changed jobs since getting pre-approved, your lender may deem you to be a risky borrower and decline your home loan application. Bottom line: avoid changing jobs or selling assets between pre-approval and applying for a mortgage. Your credit score has deteriorated If you’ve applied for other credit products since being pre-approved (such as a car loan or credit card), taken on more debt or missed repayments on existing debt, your credit score may be affected. This in turn could impact your ability to get over the line with a lender. Be mindful of managing your existing debt carefully and avoid applying for other forms of debt after pre-approval. The lending criteria has changed In some instances, changes to the bank’s lending criteria could put your home loan application on ice. If they tighten their lending conditions after you were pre-approved, you may no longer be eligible for finance. In some instances, the lender may have given you pre-approval incorrectly. For example, they may not have properly verified your information or you may have omitted information that affects your home loan application. Be sure to provide all the right documentation right from the get-go. The lender has reservations about the property Lenders may be hesitant to provide finance for certain types of properties, particularly those they suspect may be difficult to sell down the track. Examples may include inner city apartments, properties needing significant renovations and those in high-risk disaster-prone areas. Check with your lender prior to house hunting about whether they’re less inclined to lend money for certain types of properties. Interest rates have increased Say there’s an interest rate rise in the time between pre-approval and your home loan application. The lender may find you can no longer service the loan and your application may be rejected. Look into whether rate locking is an option (that is, fixing your interest rate before your home loan application is complete) to prevent this from happening. What to do if your home loan application is rejected If your home loan application is unsuccessful, you may need to: Provide further documentation about your financial circumstances Work on improving your credit score Shop around for a different lender (but don’t apply to multiple lenders in a short time immediately after a rejection, as this can negatively affect your credit rating) Stay in your current employment longer Set up a budget and demonstrate your savings ability better Find a different property. Whatever you decide to do, we’re here to help you tackle any hurdles and be approved for a home loan. Having a mortgage broker on your team can help increase your chances of a successful home loan application, as we take the time to understand your financial situation, as well as the lenders’ requirements. To chat through your finance options, get in touch today .

When you’ve been scrolling through marketing photos of a property and you finally set foot in it at an inspection, it can be easy to get swept up in the moment. Home stylists can be very clever at making you fall in love with a property. It’s their job to help you imagine yourself living there, or to imagine your ideal tenants in the property. However, before you pounce on that dream slice of real estate you’ve been eyeing off, here are some key questions to ask yourself. Are clever staging tactics trying to hide anything? Most properties are staged to sell nowadays, as vendors know they can often get top dollar for houses and units that are beautifully presented at inspection. Try to look past the cosmetics for faults and defects that could prove costly to repair later. Is a rug cleverly disguising uneven floors? Is a pot plant hiding cracks in a wall? Has wide-angle photography made the living room or bedrooms look bigger in the marketing photos than they actually are? Is the lighting covering up the fact that the property feels more like a cave? Remember, the contemporary furniture, art and décor won’t be staying once the property is yours, so don’t fall for those kinds of distractions. What renovations or modifications have been done? It’s always smart to ask about any previous renovations. This can give you a clearer picture of the property’s true value, and who knows, it might spark ideas for your own future projects. Plus, if you’re thinking of making changes later on, asking about past work can help reveal any council restrictions or subdivision limitations that could impact your plans. Why are they selling, and what price are they hoping for? Asking why the owners are selling—and how long the property has been on the market for—can give you valuable insight, especially if they’re in a rush to sell. This, paired with finding out the price they’re expecting, can help you assess if the property fits your budget and gives you the upper hand in negotiations. The more you know, the better you can shape your offer. What’s happening up top? A leaky roof or water damage can be costly to fix. Signs there could be a problem include mould on the roof, roof rot, missing or buckling tiles, damaged flashing, wavy cornices, and damp patches on ceilings or walls. Have a good look at the roof from outside the property. Check the roof gutters for rust, and make sure the downpipes run to the storm water drains. Inside, assess the ceilings for sagging. An easy tip is to shine a torch across the ceilings, which should show up any deflections and defects. Again, get a professional building inspection to be on the safe side. What’s the plumbing like? Don’t be afraid to turn on the taps and flush the toilets during the open inspection. You’ll want to listen for hammer issues and check the hot water is working. Also, ask how old the hot water system is and when it was last serviced. What’s the property’s orientation? Orientation is really important because it affects how much natural light the property will get at different times of the year. North or northeast facing properties often get the most sunlight. If the ceiling lights are ablaze during the inspection and it’s a sunny day, the house may lack natural light and you may be in for a pretty dark winter. Have you done enough preliminary research? You should always do some digging to understand more about the suburb before buying. How is the area performing? What is the capital growth like? How are comparative sales tracking and is the listed price fair? What’s the lifestyle offering like nearby and is there access to amenities? Are there any planned developments or zoning changes that could impact your purchase? Ready for a spring purchase? We’d love to line up the finance you need to get into your own home or to buy an investment property this spring. Chat to us and we’ll get the ball rolling with pre-approval today.

Buying your first home is an unforgettable experience. There’s nothing like the thrill of hearing that settlement has gone smoothly and that you own your very own home. If you’re an aspiring homeowner who is struggling to save a deposit, there may be other options to get you over the line and into your first home sooner. A guarantor loan is one of them . A guarantor loan is where a relative, usually a parent, uses the equity in their property as additional security for your property purchase. And it’s not uncommon. According to research by Digital Finance Analytics, the percentage of first homebuyers seeking help from parents jumped from 3 per cent in 2010 to 59 per cent, with the average loan for a deposit increasing from $23,000 to $107,000. Here’s what you need to know about guarantor loans before diving in. Why consider a guarantor loan? To buy a property, you usually need a 20 per cent deposit. For many people, saving a deposit of that size can be difficult and take years, particularly with today’s cost-of-living pressures. A guarantor loan offers an alternative way to get into the property market. Sometimes, a guarantor can mean being able to purchase a home with no deposit at all. Having a guarantor can also help you avoid paying Lenders’ Mortgage Insurance (LMI). LMI usually applies if you borrow more than 80 per cent of your home’s value. It’s to cover the lender against the risk of you defaulting on the loan. Who can be a guarantor? Typically, a guarantor is a close relative like a parent, grandparent or sibling who is willing to offer up their own home equity in addition to your cash deposit. If you’re unsure what equity is, it’s the difference between their property’s value and how much they (still) owe on it. How does a guarantor loan work? The guarantor doesn’t actually have to hand over any money at settlement. They simply agree to offer part of their property’s equity as security. Here’s how a guarantor loan may work. Say you wish to buy a $600,000 property and you have a 10 per cent deposit saved of $60,000. To buy the property, you need a deposit of 20 per cent, so $120,000, otherwise, you’ll have to pay LMI. Your parents offer $60,000 of their home equity as extra security for your home loan. They don’t have to make any payments at settlement, but if you default on your mortgage repayments down the track, the guarantor may be liable. Once you’ve built up equity in your home – either by paying down the mortgage or if the value of the property increases – your guarantor can be released from the loan (fees may apply). Risks to consider Before diving into a guarantor loan, it’s important to consider the risks involved. As mentioned, if you’re unable to make the repayments, your guarantor will be financially liable. Some of the guarantor’s equity will also be tied up in your property, which may affect their ability to sell or refinance. There’s also the impact of mixing family and finances to consider. It’s a good idea to seek legal and financial advice before entering into a guarantor home loan. Like to explore your finance options? If you’re hoping to buy a property and you don’t have a 20 per cent deposit saved, a guarantor home loan may be worth investigating. Get in touch today and we’ll run through the pros and cons of a guarantor loan and the different lender requirements.

There’s nothing quite like the buzz of seeing those words in your inbox: Confirmation of settlement of your property purchase. Settlement day can be both exciting and stressful. But once the formalities are done, it’s all worth it. If you’re planning a property purchase and are new to how settlement works, here’s a rundown.

Are you new to the world of property investing? If you’ve ever found yourself scratching your head at the complex lingo, we’re here to turn that confusion into clarity. Imagine dazzling your dinner guests with your newfound knowledge, effortlessly chatting about the ins and outs of the market.